The history of DeFi so far could be described as “speedrunning” finance. It’s gone through many of the same building blocks as our current financial system, progressively extending the set of “money lego” to be combined together into this new paradigm. Many of these money legos are yet to be built, we don’t have on-chain mortgages yet, don’t have a vehicle to sell a loan to a liquidity protocol like AAVE. But for anything in the traditional finance world that’s not in the DeFi world, the question isn’t “if”, but “when”.

Most derivatives products have yet to be exposed to DeFi in a serious way, these either don’t exist or barely exist in DeFi at the moment. It means that most of finance is still in traditional finance institutions. The global equities market was estimated around $38 trillion in 2019, meanwhile, the global derivatives market was worth as much as $1 quadrillion. So, for every dollar in equities, there is as much as $25 in derivatives. An assumption is that if the DeFi unlocks on-chain derivatives, it would be a massive increase in the value locked in DeFi. And the protocols that take the first bite successfully could generate insane amounts of revenue.

One of those protocols that could bring this market on-chain is Dopex. An options platform living on Arbitrum, a layer 2 scaling solution of Ethereum, since launched in early 2021, Dopex has reached nearly $100M in TVL and $700M in market cap. So, let’s breakdown how Dopex might look like in the future.

I. Project Overview

Dopex stands for the term Decentralized Options Exchange, simply put, Dopex is a decentralized options protocol which aims to maximize liquidity, minimize losses for option writers and maximize gains for option buyers, all in a passive manner for liquidity contributing participants.

Options market has historically been tough to do on Ethereum because they involve more frequent trading than just buying and holding an asset. A savvy options trader might buy a variety of puts and calls spread out across the future at different prices to hedge their exposure but doing that on the Ethereum mainnet could easily rack up thousands of dollars in gas fees. Hence, while the Ethereum mainnet might be great for a new stock market, with people buying and holding ERC20 tokens, it’s not great for a new options market. For that we needed Layer 2s. Why?

An Ethereum Layer 2 has the necessary ingredients for a robust options market, specifically:

- Abundant liquidity.

- Instant-like transactions.

- Low gas fees.

- Security.

Pieces of this puzzle have existed on alternative L1s and sidechains, but Arbitrum is the first network to provide the best blend of all four requirements for the options market. And Dopex is the first landing on.

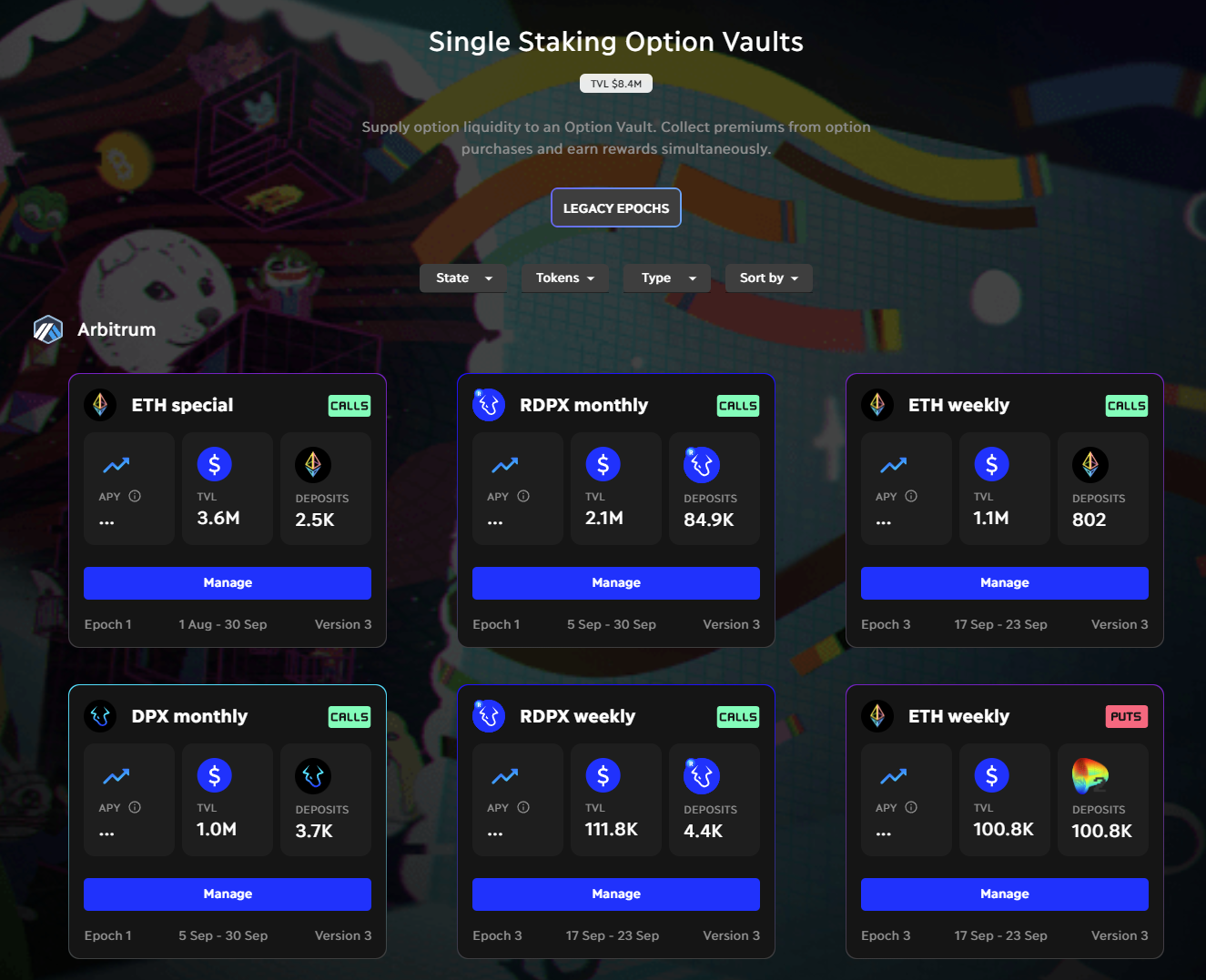

Since the options market is quite complex to trade, Dopex is building up their offerings over time. Their flagship product right now is primarily Single Staking Options Vaults (SSOVs), which provide deep liquidity for option buyers and automated, passive income for option sellers.

II. Products

SSOV

Similar to single staking vaults, SSOVs allow users to lock up tokens for a specified period of time and earn yield on their staked assets. Users will be able to deposit assets into a contract which then sells your deposits as call options to buyers at fixed strikes that they select for end-of-month expiries.

Users can do two things:

- Deposit collateral into the option pool for premium and fees.

- Buy Call Options on ETH using the liquidity provided by others.

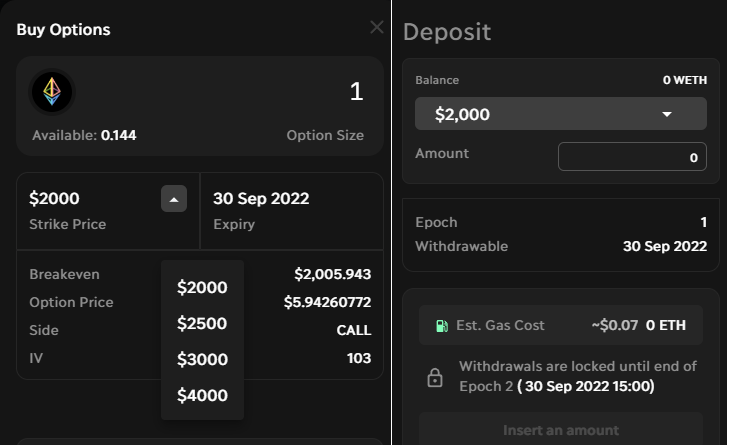

By depositing collateral into this SSOV, you’re making it possible for other people to buy Call Options. In return, you’ll earn a share of fees they’re paying of premium back to you in ETH. Currently, the SSOVs operate on monthly “epoch”, with a limited set of strike price, so you don’t have a ton of flexibility like the way of trading on Lyra.

As for personal experience, exercising an option in SSOV is a little different though. Commonly, a trader can exercise his option at its expiry date to buy the corresponding amount of the underlying asset. For example, if you buy a call option for 1 ETH at a strike price of $2,000, current price at $1,500 and ETH is at $2,500 when maturing, you will exercise it to buy the ETH at @2,000 and earn $500 in dollars.

That’s not happened with SSOV. If an option gets matured ITM (in the money), you can settle it for the difference as denominated in the underlying asset. And in the above example, you can receive $500 in ETH, equivalent to 0.2 ETH.

On the other side, the writer does not lose any asset worth in dollars. Why? The remaining 0.8 ETH at the price of $2,500 has the worth of $2,000 in dollars. Rather than, the writer earns both a premium from the call option buyer and from farming rewards from the initial deposit. Ultimately, the writer started with 1 ETH ($1,500), now has 0.8 ETH ($2,000) + premium paid + farming reward. Even the deposit expired ITM and the writer lost a portion of underlying assets, but his USD$ notional value actually goes up.

This is what makes using SSOV as a writer a little different from selling covered calls on other option trading platforms.

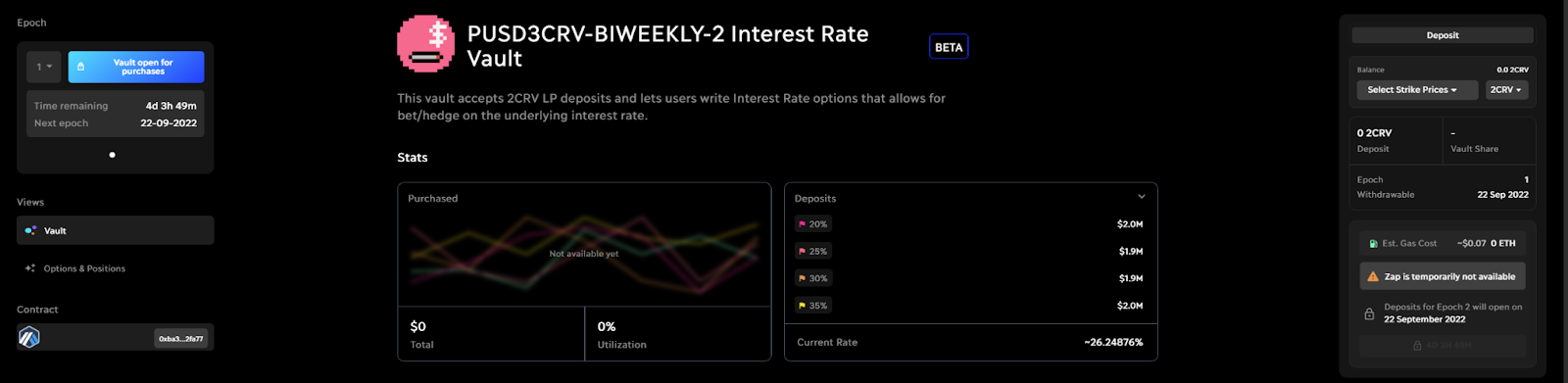

Curve Interest Rate Vault

The Rate Vault was launched but still in BETA phase, to launch options whose underlying asset is the APY of a specific Curve pool. Of course, the option is synthetically constructed as the interest rate itself isn’t a financial asset. The interest rate in Curve pool is not volatile, the platform supports up to 500x leverage.

The vault would be in the same style as its existing option vaults SSOV. If you expect a pool will get a lot of votes to raise its interest rate, you can buy a call option on that pool. If the pool APR is expired in ITM or ATM (at the money), you will profit. And vice versa, you expect less votes for a pool, buy a put option.

This product has a lot of potential, allowing users to speculate on the Curve Wars without owning CRV or related assets and especially, minimal capital, better capital efficiency. If the vault has sufficient liquidity, large players in the Curve Wars will be able to hedge or leverage their exposure, minimizing risk or maximizing profits, for a relatively low amount of capital.

In contrast, everyone can notice that there could be some serious dark side as well. Some cases, if a big player is able to control the market, he can use the Dopex options pools to fuel profit from what can only be seen as insider trading. Here for DeFi, most of the liquidity providers likely are retail investors. They will suffer.

For a better vision, interest rate options and swaps are likely to be a massive narrative incrypto in coming years. In the traditional market, it is huge and plays a vital tool for whales and institutions to hedge and de risk.

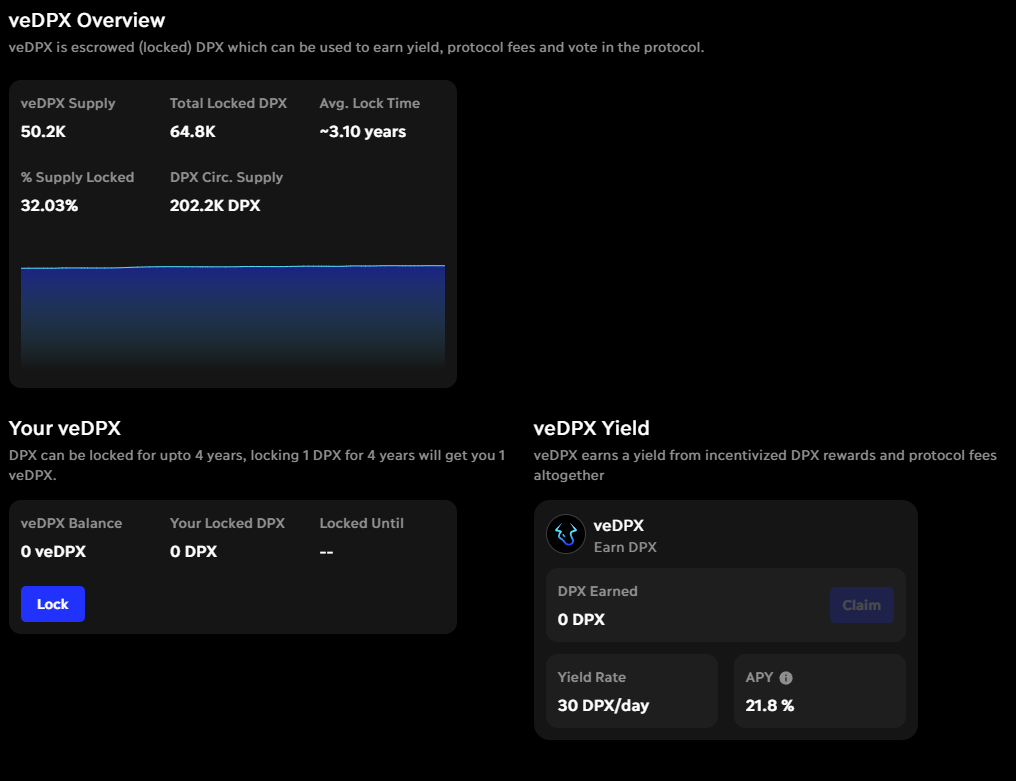

veDPX

veDPX is the staked version of DPX, being locked in a period of given time. The longer they lock their DPX, the veDPX they are given, meaning more fees. veDPX gives the holder voting rights. These will allow holders to vote on which pools the DPX token emission will go to, as well as the options strike prices. At the time of writing, the veDPX does not involve much more than expectation and its possible ability. It is likely a diluted version of veDPX to begin with, which votes on things such as pool emissions and shared revenue. Full decentralized governance will only be possible after Dopex has launched a full product suite.

There would be the multiplier for fees generated on the platform, but will this be sufficient to convince people to lock up their DPX for several years at a time? It is possible, but this could have negative effects on the price of rDPX, which could impact the protocol massively.

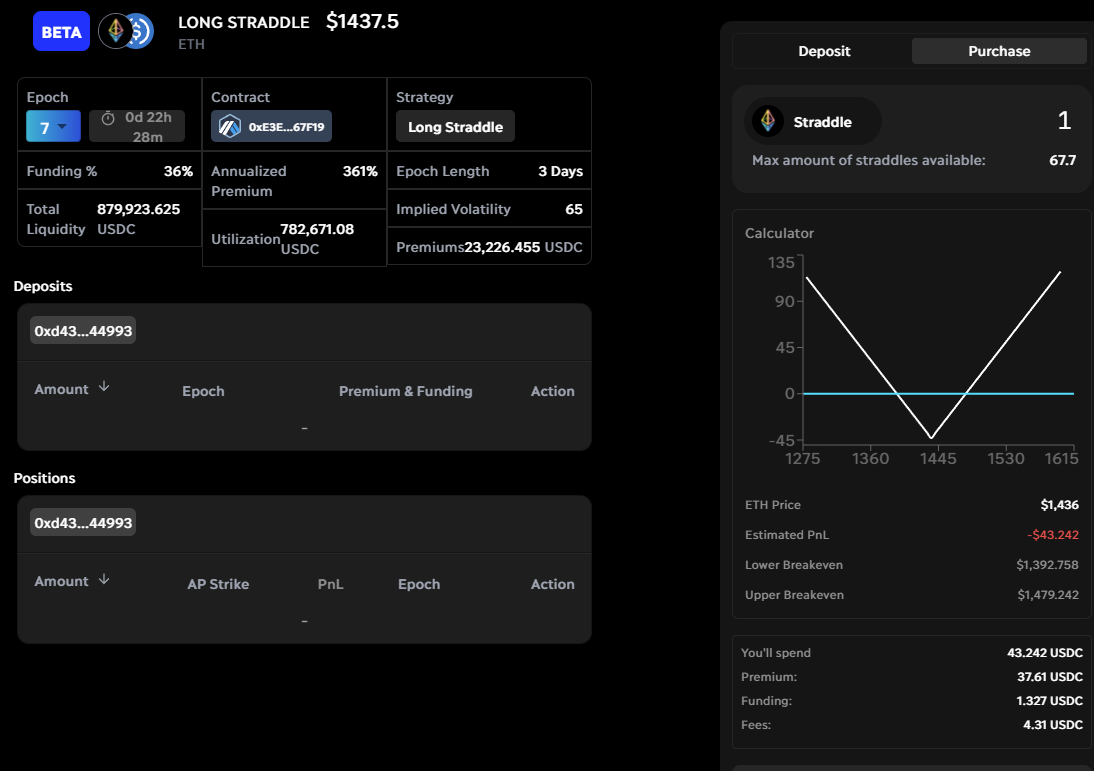

Atlantic Straddle Vaults

A straddle is a neutral options strategy that involves simultaneously buying a put and a call option on the underlying with the same expiration and strike. If the market looks volatile, you can buy these with USDC to profit from volatility in either direction. As an Option writer and betting against volatility you can Deposit USDC as collateral (sells ATM puts to the Straddle buyer). Since your selling ATM puts your only downside is if the price action is negative, if it's positive or neutral you get your deposit back +premiums and interest. Currently like ~360+% APR (no that's not a typo).

DPX Bonds

Dopex uses token bonding to incentivize users to deposit or sell their collateral to the protocol in return for discounted DPX tokens.

Only Bridgoor NFT owners can bond. It’s possible to acquire one using the TofuNFT marketplace. However, it is not clear how bonding benefits the protocol and market participants. It can be said that the amount of bonding in the treasury so far is death, but in the future, if Dopex approaches the bonding mechanism of the pioneer and its partner OlympusDAO, the demand for the bonding mechanism is probably quite large, helping the money flow through its products.

III. Tokenomics & Metrics

Tokenomics

The first thing that stands out with Dopex’s tokenomics is their two-token model. DPX is the core governance and value token, which you might buy if you want to invest in the platform. rDPX is “rebate” DPX, which is awarded to people who lose money in their options trades, and then can be used for a variety of functions on the platform. rDPX makes option trading on Dopex a little more interesting, since even if your options turn out to be losers, you still get some rDPX as a reward for playing. Get paid by being losers, sound really inconsistency.

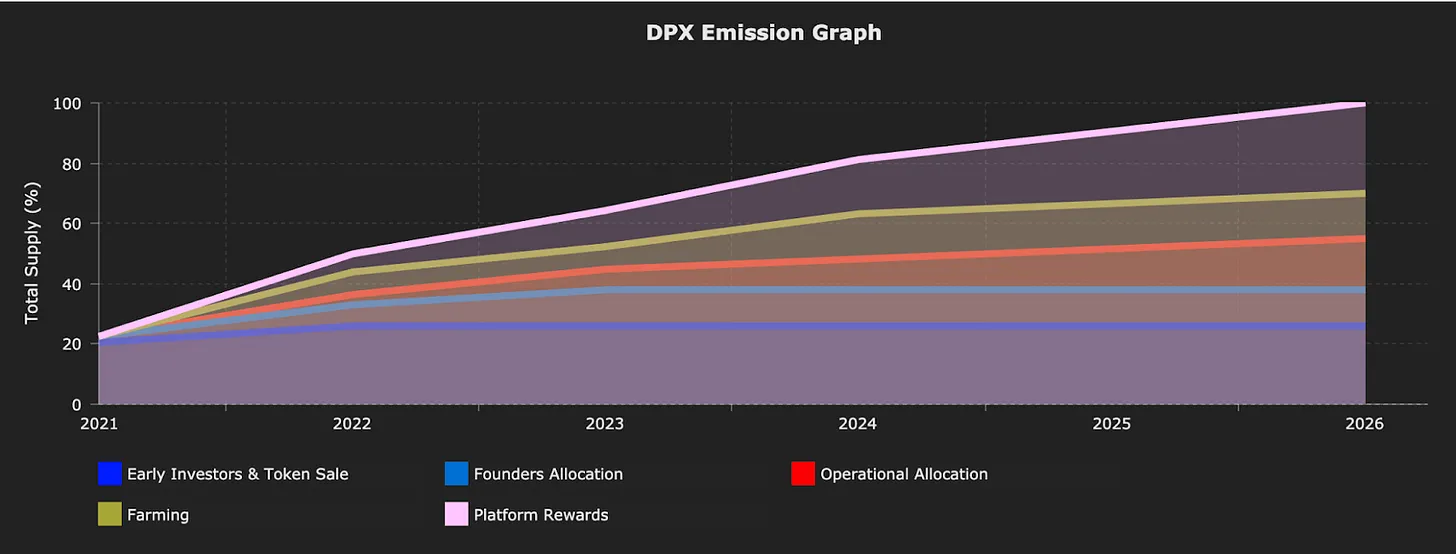

DPX has a fixed supply of 500,000 being emitted over 5 years starting in late 2021. Its two uses are to vote on Dopex governance proposals, and to earn fees from the platform. While all Dopex products allow users to earn real yields by taking on some directional risk, the protocol also generates real revenue through fees, which it redirects to stakeholders. 70% of the fees go back to the liquidity providers, 5% to delegates, 5% to purchasing and burning the protocol’s rebate token rDPX, and 15% to DPX single-sided governance stakers. Considering the potential size of their options market, it does seem as though staking DPX has the potential to generate some serious cashflow.

If DPX is the governance and fee accrual token, what’s the point of rDPX? rDPX does not have a fixed supply, so there’s no inherent scarcity to it. But it does or will have a variety of uses as the platform evolves. From their tokenomics docs again: rDPX is how you’ll pay fees for future apps such as vaults. rDPX will be usable as collateral for leveraged option positions or to mint synthetic assets. Staking rDPX will boost the fees you generate for staking DPX. These value props are honestly a little less clear. Why give away a token to people who lose money on options, which they can then use to increase the fees they earn from other people trading options? Why does this token have value to borrow against? The main value is minting synthetic assets and using rDPX for paying fees. If rDPX becomes the fee layer for Dopex, then Dopex and DPX holders earn a small additional tax on all transactions that they wouldn’t earn if everything were paid in ETH or USDC. It also has the benefit of not feeling like “real money” since you probably earned a lot of it for free, which should increase activity on the platform.

Token Metrics

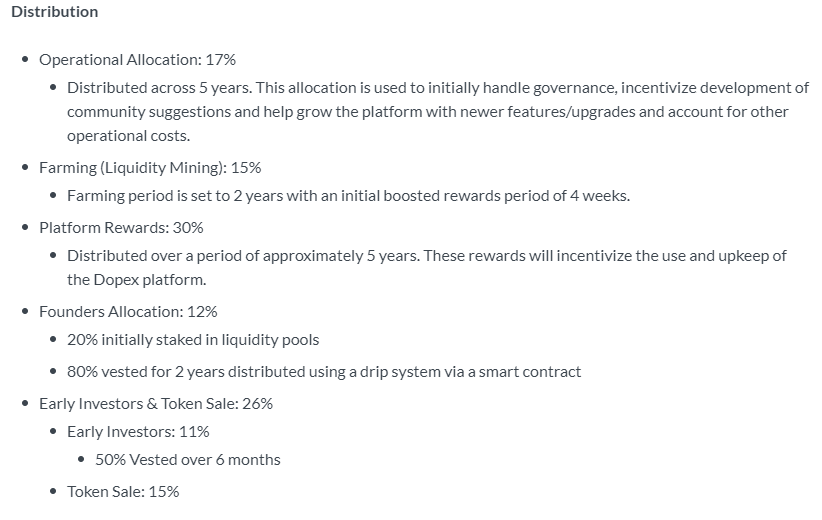

In terms of emissions and distributions, Dopex is fairly generous. Approximately 20% of their tokens were immediately released to the market, with the rest unlocking somewhat linearly over 5 years.

They did have a decent chunk go to investors, but those tokens were either immediately unlocked or vested linearly over 6 months. The team vest is also linear over 2 years. So, while there are a good number of tokens going to the team and investors, they’re being dripped out constantly instead of all unlocked at once, so there shouldn’t be any sudden sell pressure events.

Personally, when the author sees only 12% to the founders, with 45% going out to the community through use, that’s a pretty good sign. It could definitely be gamed, since the early investors and team members will have a leg up on the liquidity farming, but anyone with a decent pool of capital could acquire a large stack of DPX tokens. 17% allocated to operations over five years isn’t bad too. And the five-year emissions schedule is also promising, they’re taking their time with this.

IV. Roadmap

IV. Conclusion

Whether or not you’re interested in options trading, or investing in a platform like Dopex, there will be a few things to keep an eye on with them over the next few years. One will be how quickly they can grow the robustness of their options platform. Having a small set of strike prices with only one date is limiting, so if they can find a way to expand their options, they’ll be able to attract many more participants. Another will be how aggressively they integrate other partners who want to offer options trading on their tokens.

A lot of questions here. Will they go an Olympus Pro route and eventually offer permissionless options pools for protocols that want to enable further speculation on their tokens? They also seem to be angling to get involved in the Curve Wars, at least indirectly. What will their Redacted pools look like, and will that affect the best way to engage in the battle for Curve & Convex dominance?

Interest rate options for Curve pools certainly have a lot of potential, and we expect that interest rate options and swaps will be a big part of DeFi in the future. However, whilst interest rate derivatives themselves are vital tooling for financial infrastructure, Dopex’s ability to deliver this is certainly not guaranteed, and their future plans are very unclear, making them a risky protocol to be involved with.

In the meantime, it already offers an exciting new way to speculate on the prices of a few major crypto assets.