I. Introduction

USDC is a globally used stablecoin managed by a company named Circle. The mechanism is straightforward: people exchange their actual United States dollars for USDC, which Circle then distributes across various segments—some stored in banks, some used to purchase bonds, and some allocated for investments. Crucially, Circle's responsibility is to ensure that the reserves backing USDC never fall below the token's supply, so the bulk of the treasury is maintained in reliable banks or US bonds, the world's most liquid bonds.

Sounds risk-free, right?

Surprise! The company once faced a significant loss of over $3.3 billion from its cash reserves due to the shutdown of one of its banking partners, Silicon Valley Bank, which constituted 8% of its total reserves. This led to USDC depegging to $0.87, and it required weeks for USDC to regain its peg, aided by Circle's prompt assurance announcement.

See? Even reserve-backed stablecoins, or more aptly termed centralized stablecoins, carry unforeseen risks.

For a decentralized financial system to function effectively on a large scale, a stable asset independent of the conventional banking system is essential. This asset is vital for two primary reasons: it provides a dependable currency for transactions and acts as the main safeguard for loans and investments. Without such an asset, both centralized and decentralized trading platforms face vulnerability and instability.

The thesis above is not originally mine; they are borrowed from Ethena Labs' thesis.

This article will primarily focus on Ethena Labs, explain its mechanism in simplified terms, and offer my perspective on its product and its potential future impact.

II. Ethena’s USDe

The answer of Ethena Labs’ for the above thesis, is USDe, the “Internet Bond.”

Mechanic

Here is how it works:

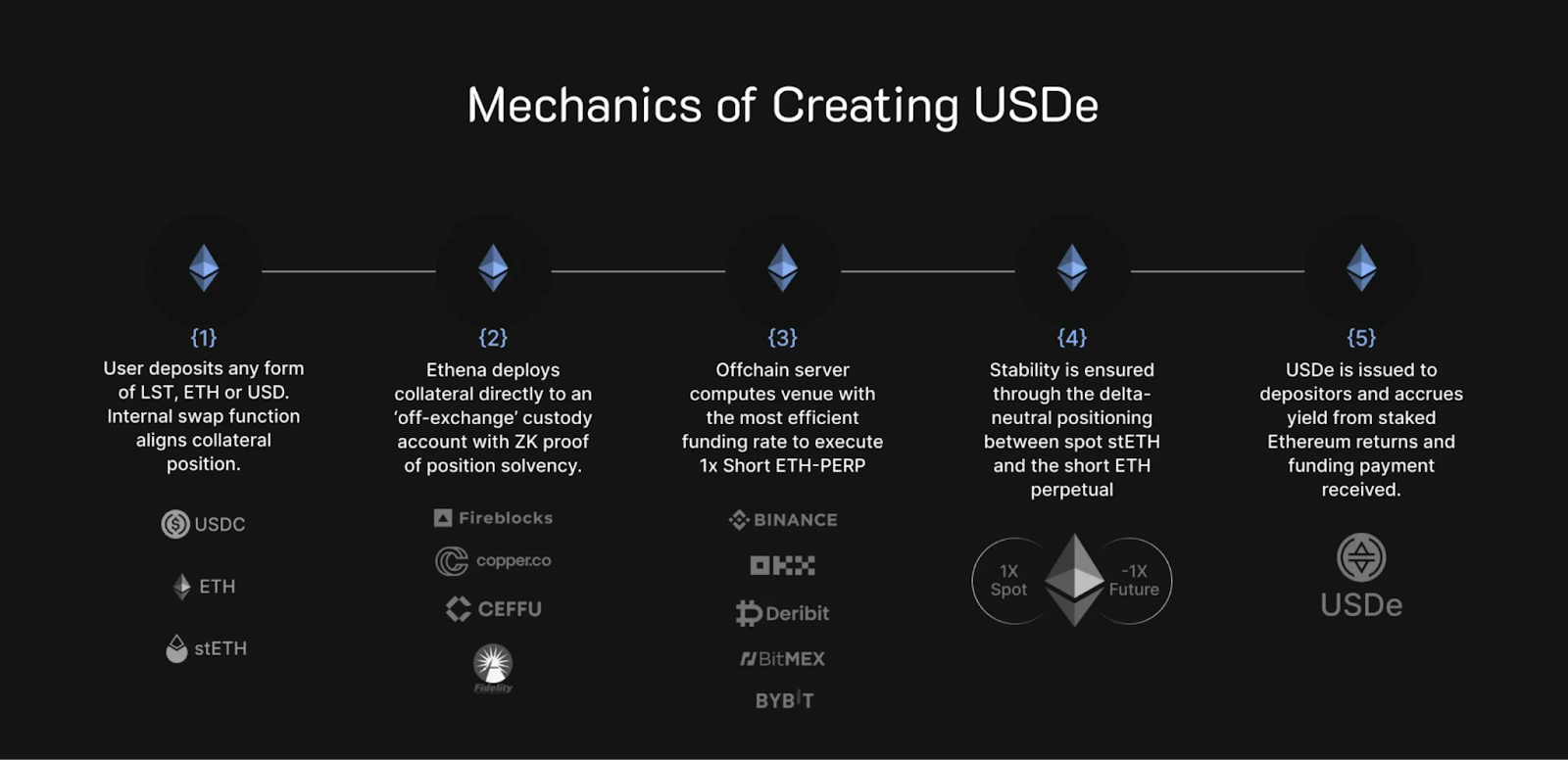

- You deposit liquidity-staking tokens like stETH, ETH, or USDC, and the protocol will turn these tokens into collateral.

- Ethena then keeps them somewhere safe from CEXs.

- Ethena will open a 1x Short ETH-PERP position on CEXs.

- Ethena’s computer will maintain the neutrality of the short position and the spot stETH.

- USDe is now sent to depositors.

That’s that simple. USDCe is backed by a smart mix of ETH investments, which are neutral ETH positions, split between 50% stETH spot and a 50% ETH short.

Yield

In simple terms, when you own or stake a bond, you usually earn a yield on it, right? The question is, how does Ethena generate this?

The profit or yield comes directly from USDe’s collateral.

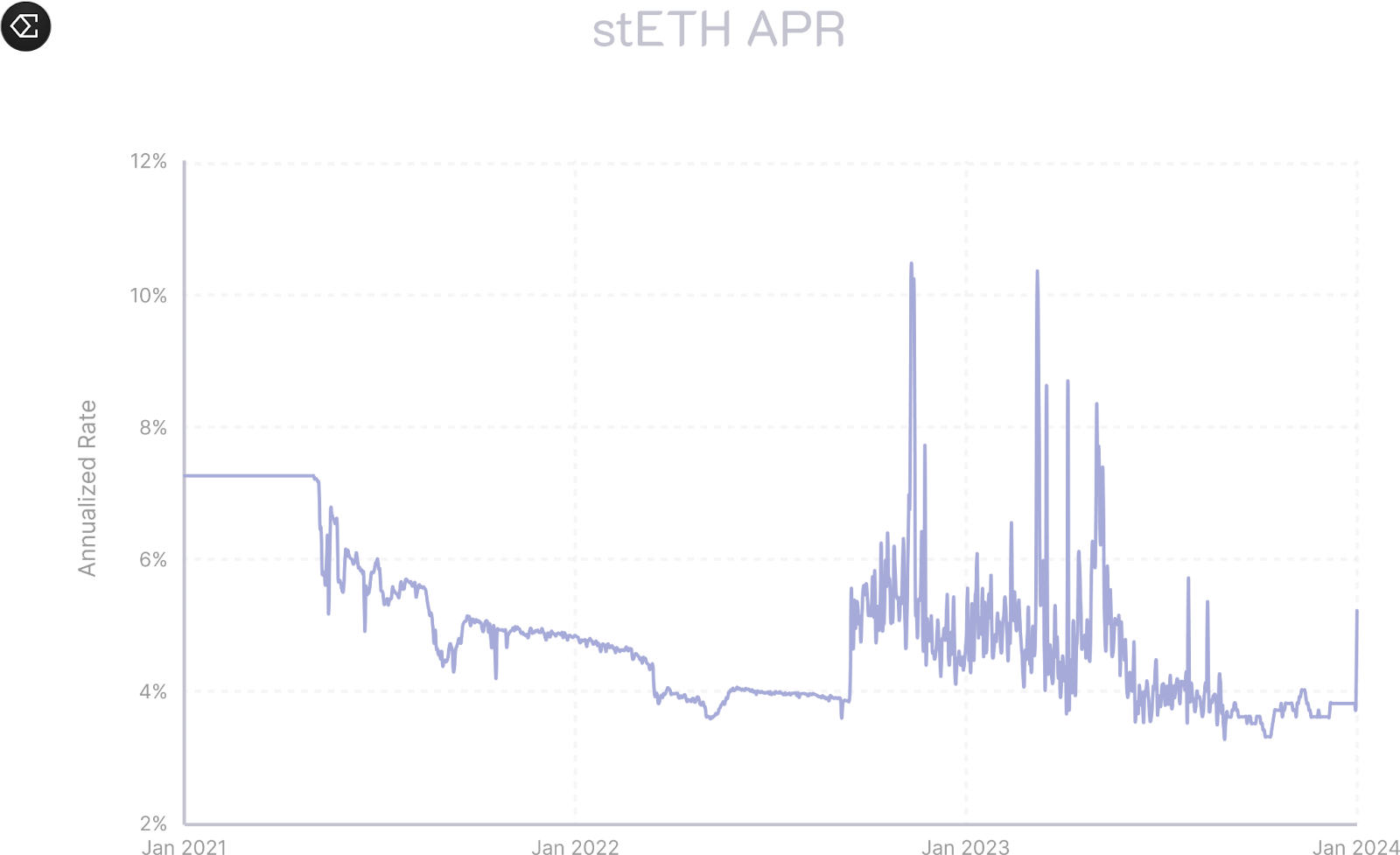

The first half of the collateral is stETH. The yield from stETH comes from three main sources:

- Inflation rewards on the Ethereum network: This is like earning interest because the network creates more ETH as a reward for participating.

- Transaction fees on Ethereum: When people make transactions, they pay fees, and a portion of these fees goes to those who stake ETH.

- Maximal Extractable Value (MEV) rewards: This is a bit more complex, but it essentially means stakers can earn extra from certain transaction order placements.

All these ways of earning are paid out in ETH. The inflation rewards are relatively stable, and the amount you can earn from transaction fees and MEV depends on how busy the Ethereum network is.

The other half of the collateral, is the ETH short position.

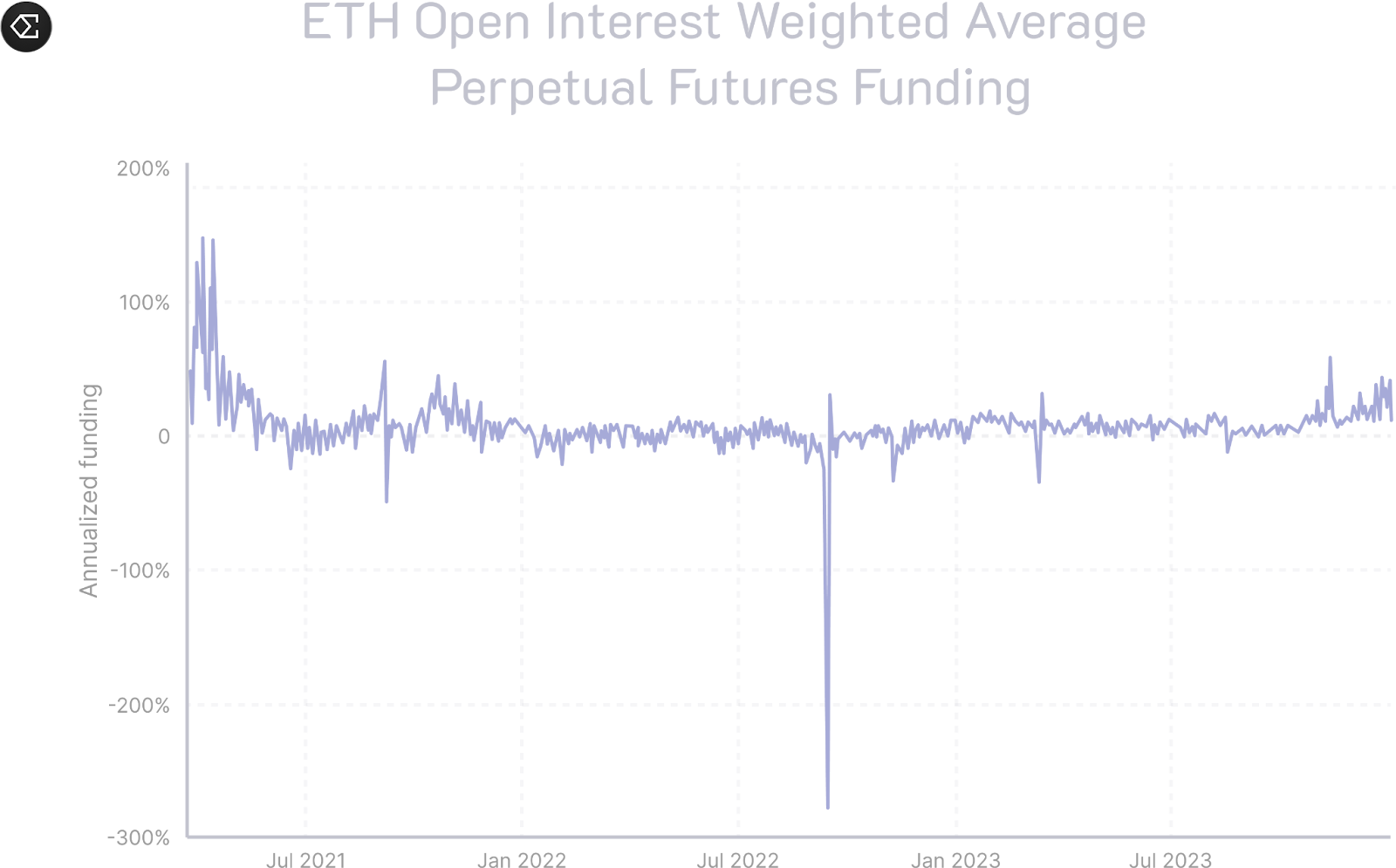

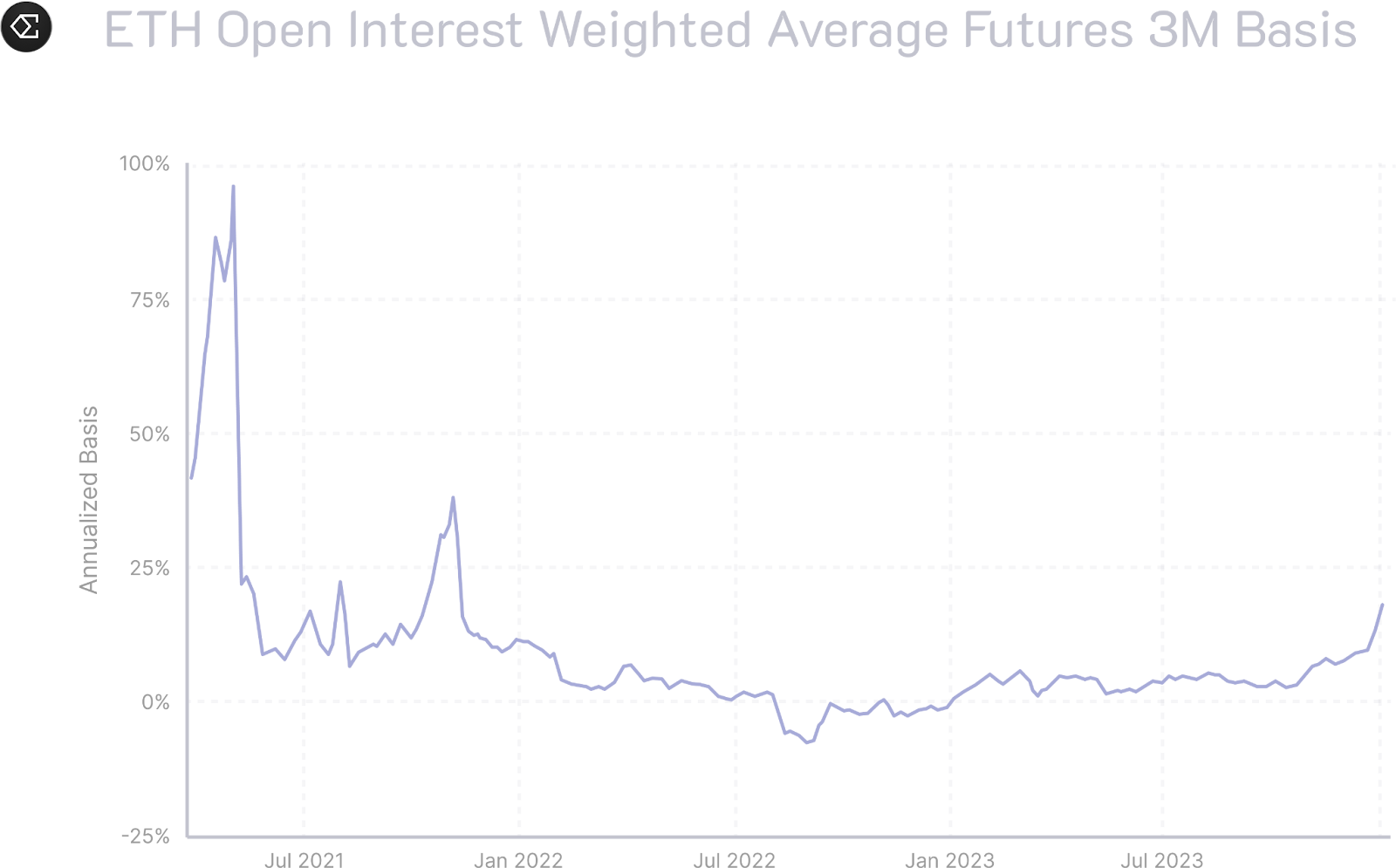

This method relies on betting against the rise in ETH's price, a strategy known as taking a short position. Historically, because more people expect ETH to increase in value over time, those who take the opposite stance- betting it will decrease - can make a profit. This profit comes from the funding fees that those expecting ETH to rise (long position holders) pay.

Assuming the long-term trend of ETH's price is still upward - even considering a timeline as extended as ten years - there tends to be a larger volume of long positions than short ones in the market, which makes the average funding rates always positive in the long run.

Ethena cleverly uses these fees paid by long position holders to increase the value of its reserve.

When combining this strategy with the yield from stETH, which ranges from 3-6% in APY, and the yield from the ETH short position, which can generate 20-25% in APY, a significant increase in the reserve's collateral value is achieved.

This over-collateralization allows the protocol to mint more USDe and distribute it to the stakers of USDe, or holders of stUSDe, creating a sustainable yield generation mechanism for USDe.

Risks

Applause to Ethena Labs, since they are one of a few projects that are open to talking about the risks involved in USDe. Here is the list:

- Funding Risk

Context: When the funding rates turn negative, and Ethena has to pay for long-position holders instead of being paid.

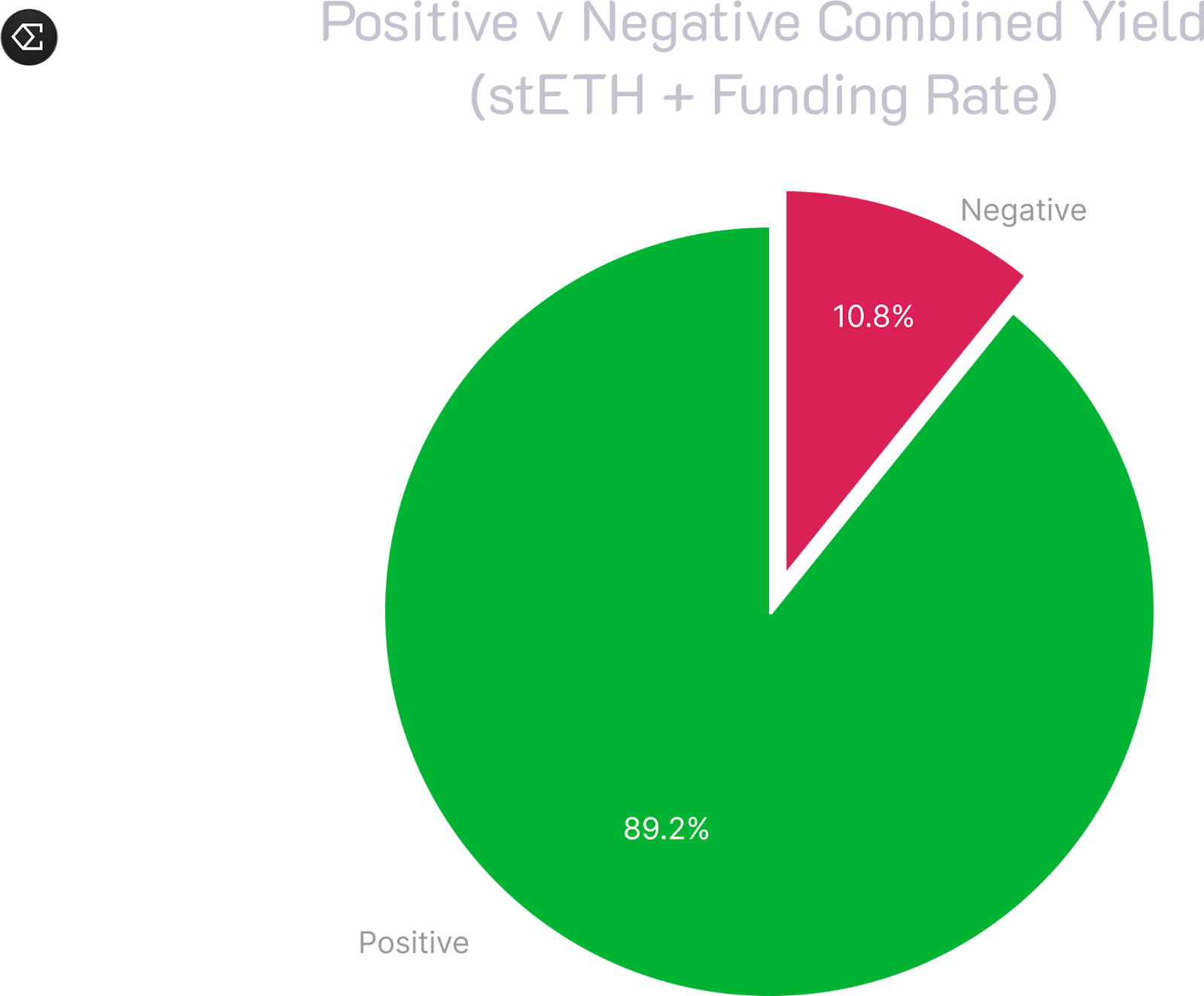

Solution: Funding rates are averagely positive in the long run. Using stETH as part of the collateral for the USDe stablecoin adds an extra layer of security through the 4-5% annual yield stETH earns. In simpler terms, the overall profit (yield) the protocol makes will only be negative if both the earnings from stETH and the earnings from funding rates together are negative.

When looking at the numbers, Ethena found that on only about 10.8% of days was the total yield negative when combining the stETH yield with the funding rate. This is a good outcome, especially when you compare it to the roughly 20.5% of days that experienced a negative funding rate without taking into account the yield from stETH.

- Liquidation Risk

Context: When CEXs liquidate Ethena’s short positions.

Answer: If there’s a risk of losing money on their bets (hedging positions), Ethena will add more money or assets to these positions to make them safer. Ethena can shift the assets they’ve put up as collateral from one exchange to another as needed. Ethena also maintains a special reserve fund that can be rapidly deployed to support its hedging strategies on exchanges.

- Partner Risk

Context: When the collateral custodians or Lido have some problems.

Solution: Depending on the problems they’re dealing with. If they’re being exploited or something that serious, there’s literally little chance to recover, though this kind of situation will be rare since Ethena’s partners are proven to be safe.

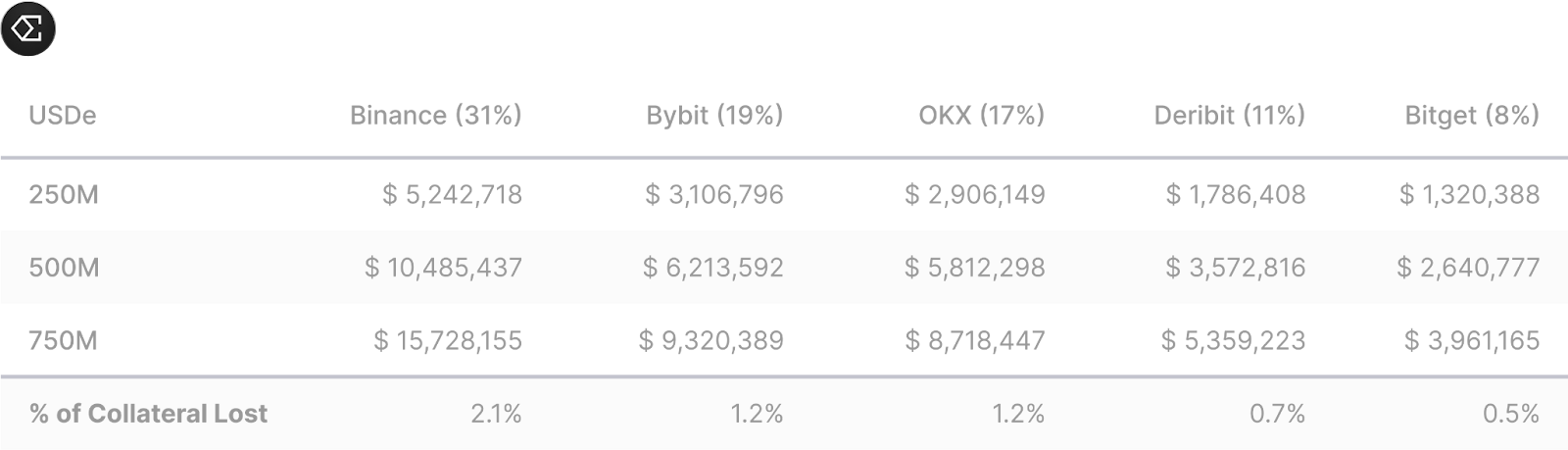

- Exchange Failure Risk

Context: When CEXs are down like FTX.

Solution: Ethena has laid out a scenario when spot prices fall 20% in the event of an exchange failure, and for different levels of USDe supply, how much profit from their short positions would be left on that exchange that fails. The maximum loss of collateral would be 2.1%, in case Binance went down, and the funding fees that Ethena received could cover this.

- Collateral Risk

Context: When LSTs, specifically stETH, are rekt.

Solution: Ethena will try to swap stETH to other assets, but the protocol will be likely to get rekt too.

Ethena has talked about all the risks so detailedly, and I believe they can resolve the situations well when crises happen. However, partner and collateral risks are the ones that can’t be resolved, and this is what investors should take into real consideration. In good times, these issues might seem unreal. But in bad times, they all happen at once.

III. USDe’s Impact

Ethena’s TVL reached $300M in just 2 days after launch. This shows an obvious FOMO from the space, but there’s still a long way to go to beat traditional stablecoins. USDT’s market cap is at $97B, and that of USDC is at $27B.

USDe might not yet have the ability to flip USDT or USDC, since these two stablecoins are so familiar to crypto folks, and people are still oriented with real-dollar-backed stablecoins. However, the essence of Ethena is still something. It brings up a protocol that all the actors involved can benefit from that.

- Ethena team gets the protocol fees.

- CEXs have more liquidity and earn some revenues.

- USDe stakers take the yields.

- USDCe users have a kind of stablecoin that's hard to block or control.

- And ETH holders benefit as ETH’s price will pump.

Let’s go deeper into “ETH’s price will pump.” The reason for this is that what Ethena and all kinds of liquidity staking, restaking projects out there are doing is a part of the same playbook: they're finding new ways to lock ETH, create scarcity, and drive up demand.

But things are far from simple. Consider this scenario:

> Buy 1 ETH with $3,000

> Stake 1 ETH for 1 stETH (TVL is now $6,000)

> Use 1stETH to mint USDe (TVL is now $9,000)

> Buy ETH again with those USDe

> Stake ETH again for stETH (TVL rises again)

> Use stETH AGAIN to mint USDe (TVL rises AGAIN)

>looping

Through this looping strategy, an initial $3,000 can be doubled, tripled, quadrupled, or even increased tenfold to $30,000, with the real backing being just $3,000.

This mechanic is why such protocols like EthenaFi, or any kind of liquidity staking, liquidity restaking, or what’s gonna be here later, liquidity re-re-re-re-re-staking, go up to millions and billions of TVL in just a short amount of time. But bubbles won’t last long. All bubbles that bring a project to Valhalla, will bring it back to dust.

Let’s say a protocol with a TVL of $1 billion, backed by a mere $100 million in initial collateral. The logic of enabling users to withdraw liquidity is nonexistent. Once people realize their wealth is delusional, a mass exit of liquidity will happen, affecting not only these bubble-creating DeFi projects but also legitimate, beneficial ones, and even ETH itself.

The model of Ethena is likely to help boost the momentum of this cycle in a crazy way, but also likely to bring it down in an unimaginable way.

Ethena's playbook might turbocharge this cycle, but it's also setting up for a crash landing that'll be one for the books.

IV. Conclusion

This article focuses solely on Ethena's USDe and how it’s gonna play out, setting aside the project's backers, team, community, and operations.

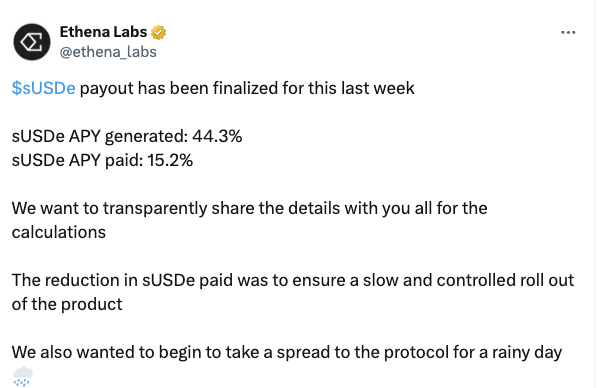

However, there’s something I gotta tell you. While writing this, the first USDe yield payout was finalized and announced on their X, and the way they distribute creates huge criticism.

The yield made was 44.3% in APY, and Ethena Labs just took 66% of that, leaving their USDe stakers with only 15.2% in APY. They shared a detailed explanation about generating yields with on-chain data but barely touched on why they kept such a large share. This really shows that USDe, though called decentralized stablecoins by the team, is not that “decentralized.”

Let’s come back to USDe’s playbook. Right at the moment I saw the model, I have an instinct of how this cycle will be crazily hyped. There are many turbochargers with great yields, and we are likely to witness the cycle of a lifetime. Many people will probably be millionaires at the peak of this bull run, but only millionaires with their unrealized PnL. The ones who could exit their liquidity, or in other words, realize their PnL in full at the right timing, are the ones going to Valhalla.

Now that I've laid out the playbook, the next move is yours. What will you decide? Remember, it's your money, and ultimately, your choice.