I. Introduction

Did Q3/2023 pull the rug from under crypto's feet or set the stage for a comeback?

As we step into October, the crypto community is actively reflecting on the events of the past quarter. Q3 was marked by a series of challenges that raised eyebrows even among the most optimistic crypto enthusiasts. In Q3 2023, the cryptocurrency market faced challenges due to regulatory uncertainty, declining market trends, and security issues. Despite these challenges, there was a notable increase in institutional interest, suggesting a maturing market. However, the overall market cap decreased, indicating a sense of caution in the market.

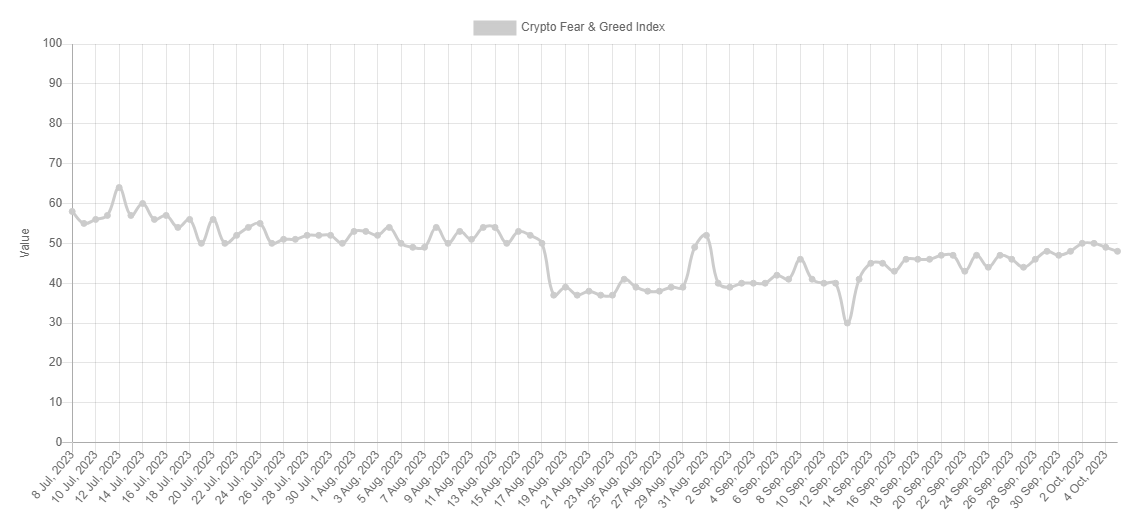

During Q3 2023, the crypto market endured a tapestry of sentiment, oscillating between optimism and caution. The Bitcoin Fear and Greed Index, fluctuating from 40 to 65, encapsulated this sentiment shift—rising to 65 in late June, reflecting a more optimistic or greedy outlook, then descending to around 40 by September's end, indicative of a more fearful or cautious stance among investors.

The turmoil in this quarter can also be linked to macroeconomics situations, such as China's significant sell-off of US Treasury bonds, totaling $124.5 billion over seven months, aimed to defend the CNY and reduce risk exposure amidst potential US trade tensions. While other nations like India, the UAE, and Brazil bolstered their US debt holdings, China's move escalated 10-year bond yields in the US to 16-year highs, echoing in Germany with yields peaking since the 2011 crisis.

This action, partly to diversify China's foreign exchange portfolio especially after the US excluded Russia from the SWIFT system, rippled into the crypto market. Rising bond yields, often heralding higher interest rates, could strengthen the US dollar, making cryptos less appealing. The increased allure of bonds as safe-haven assets could divert capital from riskier assets like Bitcoin or Ethereum, potentially driving down their demand and prices amidst a cautious investor sentiment triggered by the macroeconomic fluctuations.

In response to the turmoil, The FED decided to maintain interest rates during its September 2023. By keeping interest rates unchanged, the Fed aimed to keep inflation in check and avoid a possible economic downturn, amid global financial changes and fluctuating bond markets. This decision aimed at keeping the economy stable, and only had the crypto market fluctuate slightly.

As we explore further into the events of Q3/2023 in the subsequent sections, we'll explore these regulatory dynamics in detail, along with other significant events that shaped the quarter.

II. Price Action

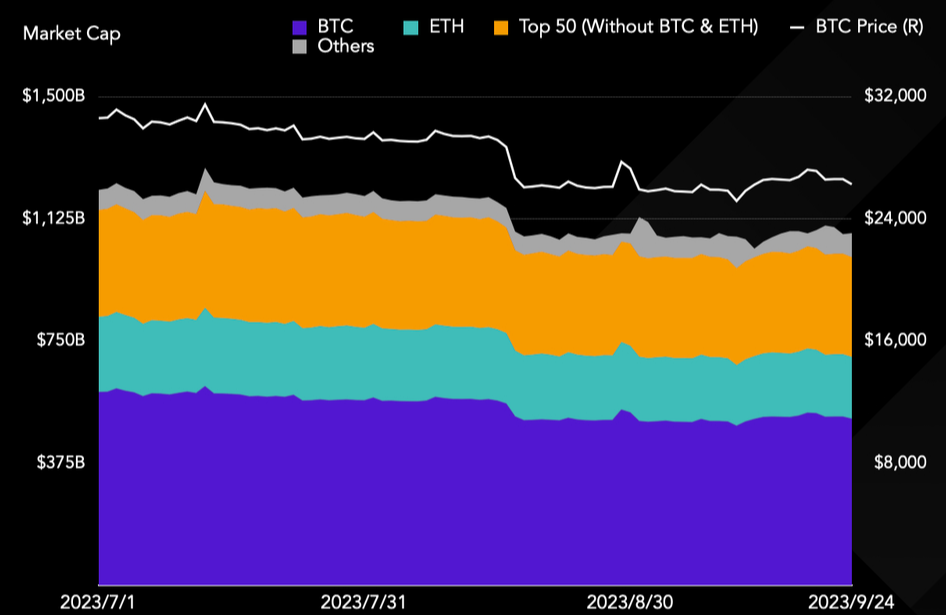

The cryptocurrency market in Q3 2023 showcased a discernible downtrend with the total market capitalization dwindling by 11% to land at $1.08 trillion. This downward trajectory was mirrored in the market caps of prominent cryptocurrencies like Bitcoin and Ethereum. Specifically, Bitcoin's market cap contracted by 14%, settling at $512 billion, while Ethereum's market cap was pared down by 18% to $190 billion.

In terms of Bitcoin’s price, Bitcoin experienced a retreat from $30,000 to approximately $26,000 over the course of this quarter. However, it's noteworthy that both Bitcoin and Ethereum have enjoyed price upticks since the beginning of the year, with Bitcoin surging by 81% and Ether ascending by 54% up to this point.

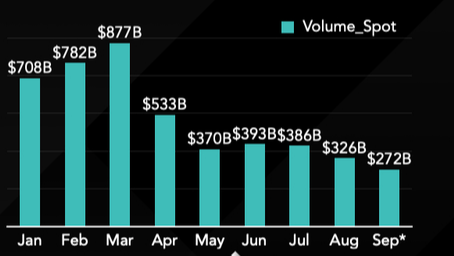

On the volume front, spot market trading volumes persisted in their decline. By September, the trading volume was forecasted to be less than $300 billion, showcasing a drop of over 40% compared to the initial volume of $700 billion at the year's onset.

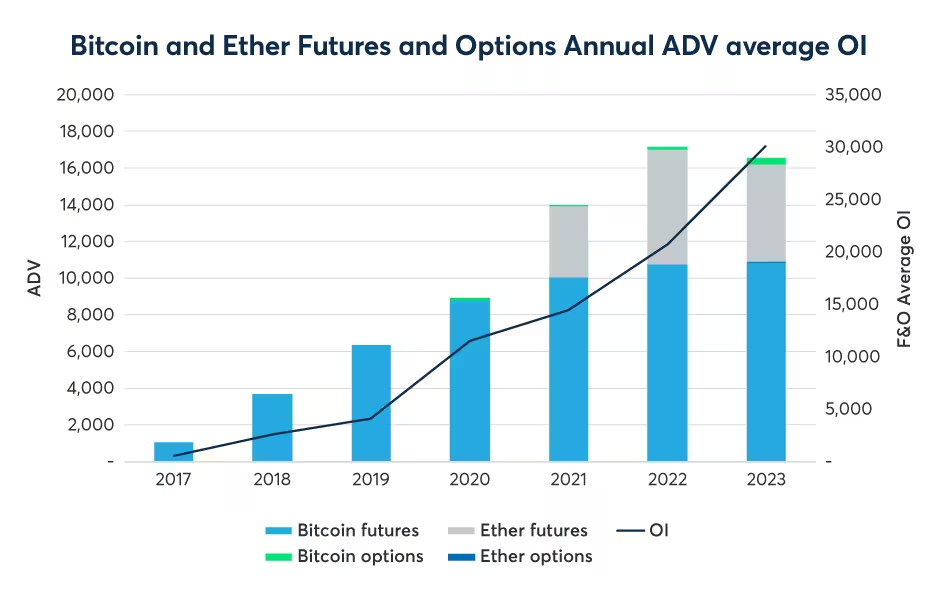

The dynamics in the futures and options segment of the cryptocurrency market told a different tale. There was an uptick in both volume and open interest across cryptocurrency futures and options offerings, hinting at a heightened level of trading activity. Elaborating on this, the average daily volume (ADV) for Bitcoin futures was logged at 10.8K contracts, and for Bitcoin options, the ADV was 345 contracts. In a similar vein, Ether's open interest (OI) for futures averaged a record of 4.3K contracts, and for options, the ADV was charted at 70 contracts.

III. Onchain Data

The third quarter of 2023 was a mixed bag when it came to on-chain metrics, and these numbers tell a story that's crucial for understanding the broader context of the crypto market.

Network Fees

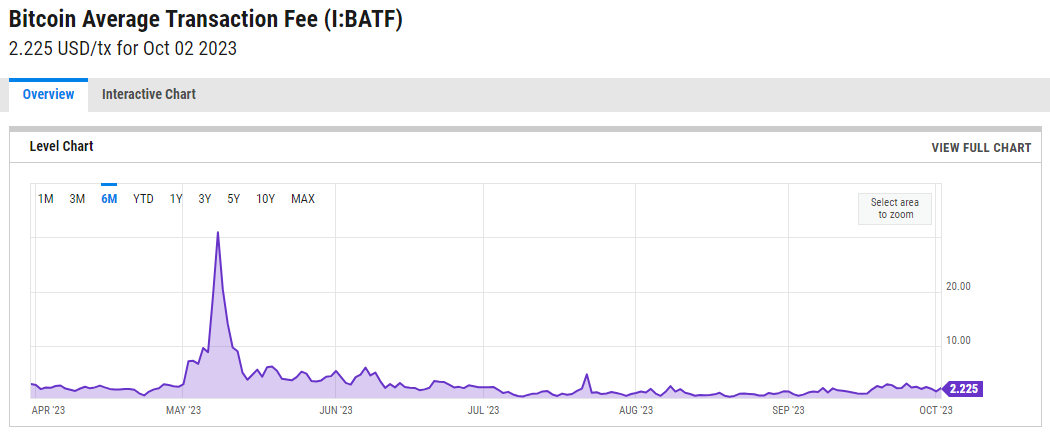

Bitcoin: The network fees for Bitcoin declined by a staggering 71.9% compared to the previous quarter. This decline was attributed to the emergence of BRC-20 tokens, which allowed for the trading of meme tokens on Bitcoin. However, when compared to Q3 of 2022, the fees have more than doubled, indicating a sustained demand.

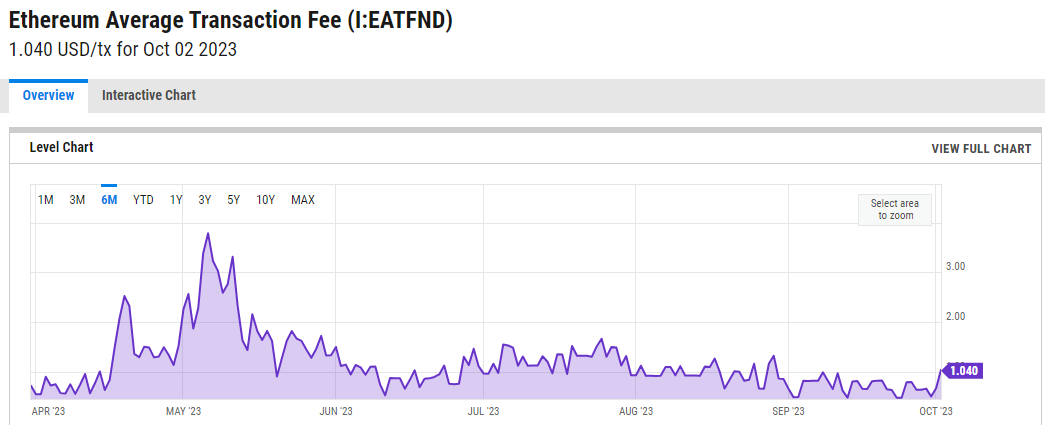

Ethereum: On the other hand, Ethereum saw a 10.8% drop in fees relative to the last quarter. This was largely due to a significant portion of transactions shifting to layer 2 solutions. Despite this drop, fees on Ethereum are up by 72% compared to the same period last year, suggesting that on-chain activity may have bottomed out last year.

Exchange Netflows

According to IntoTheBlock:

Bitcoin: The net amount of Bitcoin going in and out of centralized exchanges was relatively negligible, with net outflows of $90M throughout the quarter. This was $1.3B less in outflows than the previous quarter but $140M more than the same quarter last year.

Ethereum: Ethereum’s supply on exchanges decreased by $2.5B this quarter, which is less than the $5.5B in outflows last quarter but $1.3B more in outflows than a year ago.

Layer 2 Adoption on Ethereum

Layer 2 solutions have been gaining traction, especially with Coinbase’s recently-launched Base L2 leading the pack. As reported by L2Beat, in September, 84% of daily transactions were on L2s, compared to just 46% a year ago. While this is good for scalability, it has led to lower revenues for Ethereum.

IV. Fraud and Hacks

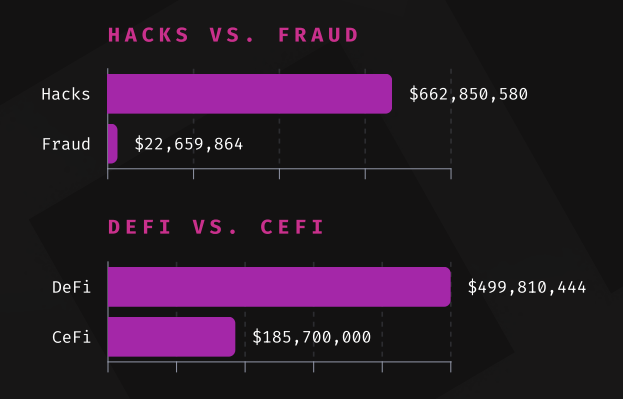

The third quarter of 2023 was a grim milestone in the crypto security landscape. According to ImmuneFi, a leading bug bounty and security services platform, the web3 ecosystem lost a staggering $685.5 million in this quarter alone. This represents a 59.9% increase compared to Q3 2022, where losses amounted to $428.7 million.

Fraud and Hacks

Hacks were the predominant cause of losses, accounting for a whopping 96.7% of the total. Specifically, $662.8 million was lost to hacks across 49 incidents. This represents a 66% increase compared to Q3 2022. On the other hand, fraud accounted for only 3.3% of the losses, totaling $22.6 million across 27 incidents—a 23.9% decrease from the previous year.

Major Losses

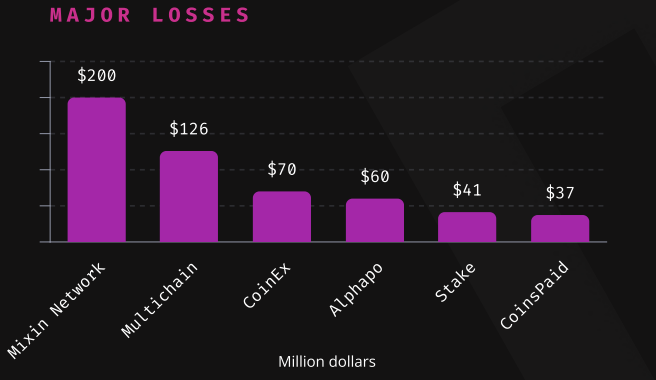

Most of the losses were attributed to two specific projects: Mixin Network and Multichain, which together accounted for $326 million or 47.5% of all losses in the quarter.

Targeted Chains

Ethereum and BNB Chain were the most targeted chains, with Ethereum experiencing 35 incidents and BNB Chain witnessing 25 incidents.

Recovered Funds

About $61.1 million has been recovered from stolen funds in six specific situations, making up 8.9% of the total losses in Q3 2023.

The alarming statistics from Q3/2023 serve as a stark reminder of the risks involved in the crypto industry. In such a bear market, developers and projects are finding ways to cash grab, making fraud and hacks more prevalent than ever, and highlighting the urgent need for enhanced security measures.

V. Trends

Telegram Bots

Since the beginning of June 2023, the crypto community has been buzzing about a new trend that has evolved into a full-blown sensation by July: Telegram Trading Bots. These bots, such as Unibot and Maestro, have redefined user experience, offering a range of functionalities that simplify the often complex and inconvenient traditional methods involving wallets and decentralized exchanges (DEXs). They have become pivotal in broadening the adoption of cryptocurrencies across the globe, offering features that safeguard against rug pulls and sandwich attacks.

In Q3 2023, written in one previous Chainslab article before, Unibot led the pack with a market capitalization of $132 million as of August. The UNIBOT token experienced a meteoric rise, surging over 1000% to $127 within just two months. Other bots like LootBot have also gained prominence, particularly among airdrop enthusiasts, quickly securing its position as the third-largest in market capitalization among Telegram Bot tokens.

SocialFi

Besides Telegram trading bots, SocialFi also turned out to be a notable trend in Q3 2023. In this emerging sector, friend.tech has distinguished itself through its unique economic model, garnering significant market attention. Within 24 hours of its launch on August 10th, friend.tech generated a trading volume of 4,400 ETH, equivalent to approximately $8.1 million. The platform has since accumulated nearly 35,000 ETH (~$60 million) in trading volume and more than $3 million in protocol fees. Its economic model, which charges a 10% fee on each group share transaction, has also been a hit, with 5% going to group creators and the remaining 5% to a treasury that has already amassed 1775 ETH.

friend.tech's success has spawned a series of clones like post.tech on Arbitrum, fan.tech on Mantle, and Friend3 on BNB Chain. These clones are rapidly gaining in Total Value Locked (TVL), making the SocialFi space more competitive. Despite the influx of developers drawn to this lucrative sector, friend.tech maintains a considerable lead, thanks in part to its first-mover advantage and endorsements from industry heavyweights like Brian Armstrong.

VI. Regulations

SEC's Increased Enforcement

The SEC, under the leadership of Gary Gensler, ramped up its regulatory actions, focusing more on courtroom battles than policy formulation. This included lawsuits and enforcement actions against entities involved in ICOs, stablecoin issuance, governance tokens, NFT minting, and trading of what were considered unregistered securities. Notably, these actions extended to crypto exchanges and market makers, including Coinbase, the only registered and publicly traded crypto broker-dealer in the U.S.

- SEC Decision on Spot Bitcoin ETF Applications

The SEC has postponed decisions on all spot Bitcoin ETF applications again, pushing the timeline into January.

- Bitwise Ethereum ETFs Launch

Bitwise Asset Management launched two Ethereum-themed ETFs, providing investors with exposure to CME Ether futures in a regulated ETF format for the first time.

- SEC's Stance on Ethereum ETFs

The SEC demonstrated a more favorable stance towards Ethereum ETFs compared to previous years. They approved nine Ether Futures ETFs, marking a significant regulatory milestone and reflecting growing interest in the Ethereum space.

- VanEck Ethereum Strategy ETF

VanEck revealed plans for an actively managed ETF focused on Ether futures contracts, representing another step towards traditional financial instruments embracing crypto assets.

- Grayscale's Effort

Grayscale Investments filed for SEC approval to convert its Ethereum Trust to a spot Ether ETF, indicating a move towards offering more regulated Ethereum-based investment products.

Summary

Q3 2023 has been a pivotal quarter for crypto regulations, particularly in the U.S. The SEC has been notably active, intensifying its enforcement actions and delaying decisions on Bitcoin ETFs. Despite these delays, the sentiment is that ETF approvals are inevitable. Additionally, the SEC has demonstrated a more favorable stance towards Ethereum, approving multiple Ether Futures ETFs. These developments indicate a maturing, yet complex, regulatory landscape for cryptocurrencies in general.

VII. Personal Thoughts

Overall, the on-chain data for Q3 2023 paints a rather bleak picture. Gas fees have plummeted, and there are significant outflows in both Bitcoin and Ethereum. Trading volumes are also considerably lower than at the beginning of the year, and the market cap is on a downward trend.

The last quarter was particularly concerning in terms of hacks and frauds. While the official statistics suggest that 96.7% of the losses were due to hacks and only 3.3% were frauds, I personally believe the reality could be the opposite. Many of these so-called "hacks" are likely internal jobs, as developers and project teams are running out of cash. In a bear market, the quickest way to make money is to exploit one's own product and defraud users. As long as the bear market persists, I expect more of these incidents to occur. So, if you have assets in any DeFi platforms, exercise extreme caution.

As for the SEC's stance on Bitcoin ETFs, it's worth noting that Gary Gensler has previously stated that Bitcoin is not a security, which technically means it shouldn't fall under the SEC's jurisdiction. Despite the SEC's attempts to delay decisions on Bitcoin ETFs, I believe approval is inevitable.

In terms of trends, Telegram trading bots like Unibot and Maestro are revolutionizing how users interact with DEXs, making the process more convenient and user-friendly. I see this as a silent revolution in the crypto industry. On the other hand, I'm skeptical about the future of SocialFi platforms like friend.tech. Their economic model appears to be a Ponzi scheme, benefiting only the creators. However, every bull market starts with schemes like this, and with the Bitcoin halving approaching, friend.tech could potentially trigger the next bull run.

Looking ahead to Q4, precise predictions are challenging to make. I have a tempered outlook for Bitcoin (BTC) given the Bitcoin halving event is just 7 months away. I expect a slow and steady rise in BTC value, rather than a sharp surge. On a broader economic scale, the US and some European countries have been tightening their monetary policies throughout the year. I suspect they'll soon lower interest rates, which typically bodes well for assets like Bitcoin.

As for market trends, I think friend.tech or SocialFi in general will still gain some attention in Q4. I believe they have a solid standing and won't easily falter. A term I expect to hear more about is Account Abstraction, specifically Account Abstraction Wallet. This technology requires a proper R&D stage, suggesting only teams whose products that truly offer value will make a mark.

Following the Celestia airdrop, I'm keeping an eye on other Layer 2 solutions like Manta, zkSync, or Starknet. While they might not have airdrops in Q4, it could be a time for their snapshots. It's all speculative, but these are the elements I'm watching as we move into the next quarter.

Right now, the most prudent approach is to stay well-informed. Awareness of risks such as hacks and frauds is essential for asset protection. Additionally, keeping an eye on emerging trends like Telegram trading bots and SocialFi can provide valuable insights. Regulatory developments should also be closely monitored due to their significant impact on market prices. In essence, being informed is the most effective strategy in this uncertain landscape. To stay ahead of the curve, make sure to keep up to date with Chainslab for the latest insights and analyses.